| « Back to article | Print this article |

Harjot Singh Narula explains the basics of paid up insurance policies

Ravi, a 32 year old businessman had bought a life insurance policy five years ago. With two kids and his wife in the family, he knew how to financially secure their future. Ravi was regularly paying the premium of the policy from past five years and was aware about most of the terms and condition of his policy.

This year due to loss in business and dispute with his business partner, Ravi forgot the premium payment date and even missed the grace period of the policy, due to which his policy lapsed. Very much disappointed he thought he had no other option but to surrender the policy. But he didn’t want to do that.

The big news came for Ravi when his agent told him that his policy was eligible to be converted into a paid up policy, which meant his policy will continue with lower sum assured and without paying any further premium.

Let us then understand what a paid up policy is all about.

What is a paid up insurance policy?

If you don’t pay the premium of your life insurance policy on time and if it lapses, then the policy becomes a paid up policy and acquires a paid up value.

In such cases the sum assured is reduced appropriately and is given to the policyholder after the completion of the policy term or on death whichever is earlier.

A policy can turn paid-up after paying premium for a minimum number of years. For traditional endowment plans it is for two to three years and for unit linked investment plans (ULIPs) it is for five years.

After the payment of premium for the specified number of years (according to policy terms and conditions), the policyholder doesn’t need to pay anymore premium and the policy continues. The insurer has no right to cancel the paid up policy unless the policyholder doesn’t choose to cancel it.

In case of participating plans, you will not be able to accrue guaranteed benefits and the bonus after converting it into a paid up policy. The policy which has an investment or savings element in its framework can only be converted into paid up policy.

Paid up value is not applicable to term insurance plans as term plans are pure protection plans which offer only death benefit.

When should you convert your policy into a paid up?

Mis-selling

Mis-selling is when you buy an insurance policy from an agent or broker where a wrong product is sold to you for better profit. Instead of selling insurance based on the needs and conditions of the buyer, the agent sells policy according to her/his commission.

If you are a victim of mis-selling and stuck with a wrong policy, then you can convert your policy into a paid up policy.

Financial limitations

Our financial status keeps changing as we progress in life. The plans which you made in the past may start looking unfeasible at the present due to some financial limitations. You can plan for a better future, but you can never predict it.

If you are in a situation where paying the premium has started becoming a financial burden for you and you are no longer willing to pay the premium, you can convert your life insurance policy into a paid up policy.

Wrong policy

Buying a wrong policy doesn’t always happen because of the agent, but it can also happen because of your lack of awareness. Many people buy life insurance policy without even understanding its terms and condition which ends up in financial burden as the policyholder keeps on paying premium for a useless policy.

In such situations, you can easily convert your life insurance policy into a paid up policy.

How is it different from surrender?

Status of the policy

One of the basic differences between a paid up policy and surrendering your policy is the status of your policy. After surrendering the policy, the contract between you and your insurer is terminated and thus the policy which you are having ceases.

You are no longer covered under the policy after surrendering it while after converting your policy into a paid up policy, you only stop paying the premium while the policy still continues with a reduced sum assured which is given at maturity or on death.

Amount received

The amount received in both the cases is also calculated differently. Both the options have different basis for calculating the sum assured and thus surrendering and converting a policy gives us different results. You should know which option will give you the maximum benefit.

The amount received in a paid up policy is known as paid up value while the amount received after surrendering your policy is known as surrender value.

How paid up value is calculated?

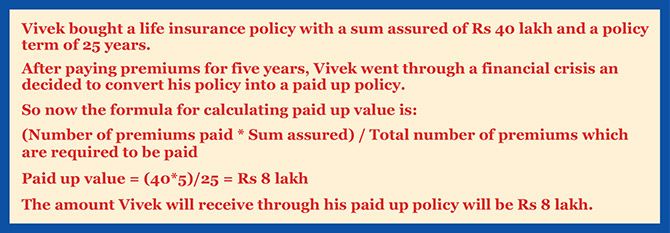

A paid up value is paid in the case of a paid-up policy at the time of maturity or on the death of the policyholder. The paid up value is always less than the actual sum assured at the time of issuing of the policy.

The paid up value is calculated by multiplying the number of years the premium is paid towards the policy with sum assured and then by dividing it with a total number of premium which is required to be paid during the policy term.

Let us understand this with an example.

Conclusion

Converting your life insurance policy into paid up policy is a decision which can be taken in case of mis-selling, inability to pay further premiums due to a financial crunch, or in case you have opted for a wrong policy. But you need to keep in mind that for converting your policy into a paid up policy, you firstly need to pay premium for a minimum number of years, as specified.

But it is always beneficial to continue your life insurance policy till the complete tenure. It not only offers you creating a surplus fund, but also allows your family a financial protection against unforeseen eventualities which is of prime importance.

Photograph: Bastian Sander/Creative Commons

Harjot Singh Narula is founder and CEO, ComparePolicy.com

![]()