| « Back to article | Print this article |

If your child is 20 when s/he decides to pursue higher eduction and her/his current age is 3 years, then here's a plan for you...

Having a child is very exciting and rewarding, especially seeing them grow up. It is a joy to watch them grow into confident young teens. There is however, a very important aspect that needs to be considered: their education. Let us look at a few ways in which you can plan for your child's education.

One should also plan and invest for not only the child's immediate requirements, but also for their education. The earlier one starts planning and saving money for this essential part of their child's life, the larger the corpus is likely to be when it is actually needed.

The most important thing to remember is to start saving very early. It is advisable to start saving for a child as early as possible, or at least at the time you are planning to have a child, as this will reduce the burden of having to save more once the child is born, due to the power of compounding.

A strict budget should be made and maintained, to ensure that adequate money is saved each month and unnecessary expenses are eliminated. This budget should include the future cost of education taking into account the rate of inflation, also one should keep in mind that interest rates can go up in the future. So creating a budget that includes the current costs as well as the potential future costs gives one a clear idea on how one should manage their finance for their child's education.

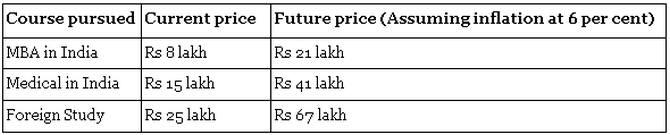

For example, if your child is 20 when s/he decides to pursue higher eduction and her/his current age is 3 years, the cost of education could look something like this:

One should consider the various investments already made, such as PPF, mutual funds, etc., for this purpose, and deduct it from the total corpus required. For example, if there is already an investment worth Rs 20 lakh in various instruments, then the total funds required (assuming foreign study in our example above) would be Rs 47 lakh, which can be amassed over 17 years.

The longer one can save for their child's education, the more the investment avenues that can be used with lower risk. For example, if one has over 20 years to save then one can look at equity mutual funds (ideally mid and large cap funds) or even direct equities which will give good returns over this time horizon. Another investment avenue for the long term is the child insurance plan which is a relatively safe option and gives protection against any uncertainties.

For shorter time periods, the best investment avenues are debt and gilt funds, which protect capital but give lower returns. It is wise to keep in mind that the longer one waits to save, the more one has to save. One should also keep in mind inflation, as this will erode the value of any investments, i.e. if the inflation is 7 per cent and the rate of return on the investments in 12 per cent, the actual return one can earn will be only 5 per cent (12 per cent - 7 per cent = 5 per cent). This should be factored in while deciding the investment avenues and time horizons.

For example if one invests Rs. 10,000 each year at 10 per cent interest per annum, the corpus will be as below:

One should also keep in mind that apart from saving for the child - be it for immediate expenses or for their education -- an adequate amount of money should also be set aside for one's own retirement. It is essential to plan your finances carefully to ensure that your retirement planning is not significantly affected by the extra savings required to bring up a child.

A blessing in disguise is that although the cost of higher education is a pressure on the family budgets and parents are forced to borrow for their children's education -- there are some tax benefits too. The interest paid (not the principal amount) on an education loan is fully deductible from taxable income under Section 80E up to eight continuous years, starting from the year in which the interest is first paid. This can be claimed by either the child (if the loan is in their name) or by the parent. A parent can also claim a deduction of payment made for tuition fee to any university, college, school or any other educational institution.

Summary:

Anil Rego is the founder and CEO of Right Horizons, an investment advisory and wealth management firm that focuses on providing financial solutions that are specific to customer needs.

![]()