Photographs: Reuters A K Bhattacharya

Twenty years ago, on July 2, 1991, the national print media splashed on its front pages what would rank as one of the boldest steps a minority government ever took in less than 10 days after its formation.

It allowed the Indian rupee -- long considered a symbol of India's economic pride -- to depreciate 9.5 per cent to take its exchange value vis-a-vis the United States dollar to Rs 23.

That also marked the beginning of a series of bold measures the government took to bail the Indian economy out of its worst balance of payments crisis and usher in reforms in industrial, trade and fiscal policies, which laid the foundation of the sustained high growth the Indian economy has experienced since.

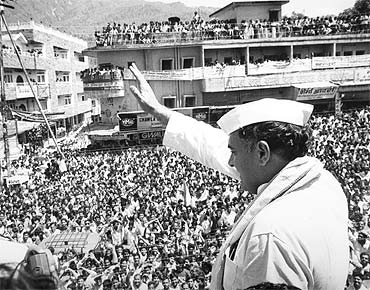

Barely 10 days prior to the currency depreciation, P V Narasimha Rao had taken oath as the prime minister of the first Congress government that did not enjoy a majority in the Lok Sabha on its own.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

At the swearing-in ceremony for the new council of ministers held at Rashtrapati Bhavan's Ashoka Hall, Rao sprung a surprise on the nation when he invited Manmohan Singh, who was then the chairperson of the University Grants Commission, to become a Cabinet minister. A day later, he was named the finance minister.

Singh walked into his new room in North Block realising fully well that this was his biggest challenge in a long career that had seen him occupy virtually all important positions in the country's economic administration -- chief economic advisor in the finance ministry, secretary in the economic affairs department, member-secretary and later deputy chairman of the Planning Commission and governor of the Reserve Bank of India.

How serious was the crisis? On the fiscal side, India's deficit had grown to 8.4 per cent of gross domestic product, or GDP. That was perhaps still manageable.

However, the bigger worry was on the balance of payments front -- the country's foreign exchange reserves were hovering at $1.3 billion to $1.5 billion (today the reserves are over $300 billion) and that was not enough to meet the country's import needs for even three weeks.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

The total external debt was $70 billion. For an economy whose GDP was under $290 billion the burden was huge, even though only $4 billion out of that had a short-term tenure.

India's international credit rating had taken a hit. The World Bank and the International Monetary Fund were reluctant to sanction new loans unless the new government convinced them of its commitment to reforms.

Signs of the crisis had become evident much earlier.

In September 1990, the National Front government of VP Singh had anticipated trouble.

It approached IMF and borrowed about $550 million under the gold tranche facility, without making any public disclosure. However, no corrective measures followed to improve the balance of payments situation.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

The situation got worse when the National Front government fell and Chandra Shekhar formed his minority government with Rajiv Gandhi's support in November 1990.

By January 1991, the Chandra Shekhar government, with Yashwant Sinha as the finance minister, convinced IMF to approve two loans -- $775 million under the first credit tranche and $1.02 billion under the compensatory and contingency financing facility.

The promise the government made to IMF was that it would initiate economic reforms through the Budget it was due to present in February 1991. By the middle of February, Rajiv Gandhi's Congress withdrew its support to the government which therefore was in no position to present a full Budget on February 28 as it had planned.

Elections were called -- a long process that would be over only by the end of May. With no government likely to be in place before June, India's economic crisis worsened.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

On April 28, 1991, India's finance secretary, Sriranga Purushottam Shukla, and RBI Governor S Venkitaramanan were in Washington.

It was that time of the year when IMF and the World Bank hold their annual spring meetings. Both the Bretton Woods institutions were unhappy with India for its failure to honour the promise of reforms because of political reasons.

Now they saw India's finance secretary seeking their help in convincing members of the Aid India Consortium to offer some temporary loans to bail out the country.

Shukla sought a $700-million bridge loan from members of the consortium -- the United States, Japan, Germany, the United Kingdom, France and the Netherlands.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

A few days earlier, Sinha had visited Japan to seek financial assistance. Foreign secretary Muchkund Dubey too was in Washington to persuade the US to tell Japan and Germany to come to India's rescue.

India's lobbying had some impact as a few days later Japan extended a soft loan of $150 million with a further commitment of $350 million, Germany granted a loan of DM 685 million (equivalent of $400 million) and the Netherlands offered $30 million.

While this kept the foreign exchange reserves above the critical level of $1 billion, trade and industry faced an acute import squeeze.

State Trading Corporation and MMTC, the biggest trading arm of the government then, began cancelling import orders.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

Worse, foreign suppliers were now refusing to honour letters of credit issued by Indian banks, unless internationally reputed banks guaranteed or confirmed them. This obviously raised import costs.

The Chandra Shekhar government also took a series of tough belt-tightening measures. On May 3, the Reserve Bank of India introduced 10 per cent cash reserve ratio on incremental net demand and time liabilities, raising the total CRR requirements to 25 per cent.

The money market became tight with call rates going up from 30 per cent to 40 per cent. A week later, the government imposed fresh curbs on credit expansion by imposing a 25 per cent surcharge on bank credit for import finance.

As the crisis deepened, the government realised it had no option other than seeking an early IMF loan. On May 13, a two-member team comprising Chief Economic Advisor Deepak Nayyar and RBI Deputy Governor C Rangarajan left for Washington.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

Their objective was to press for a $700-million bridge loan to ensure that India did not default on its international payments obligation.

The situation was so serious that all senior political leaders across different parties had agreed on one central issue: the country had no option other than seeking an IMF loan and the leaders who spoke in favour of an IMF bailout included Rajiv Gandhi, LK Advani, VP Singh and Chandra Shekhar.

Tragedy struck India soon thereafter. Rajiv Gandhi's assassination on May 21 plunged the country into an even bigger crisis.

The remaining rounds of polling had to be rescheduled and it became clear that the new government would not be in place before the end of June.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

Even as the World Bank and IMF issued statements reaffirming their support to India, it was clear that no fresh loans from either of the two institutions or the other rich donor countries would come before the end of June.

With the foreign exchange reserves going below the critical $1-billion mark, the Chandra Shekhar government took perhaps the biggest step that any caretaker government had taken -- it decided to sell 20 tonnes of the confiscated gold it had in Zurich with the option of buying it back after six months.

In return it obtained a loan of $240 million. The sale of gold took place on May 30 and the entire operation, cloaked in secrecy, was conducted by State Bank of India.

The nation got to know of the gold sale only after a week. Once Sinha confirmed the sale, political parties did not hesitate to criticise the move, little realising that there was no other way if the government had to avoid a default on debt repayment.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

Even Congress leader Pranab Mukherjee issued a statement criticising the gold sale.

Meanwhile, India's credit rating suffered further in the international market. Standard & Poor's downgraded India's long-term rating to the speculative category as it reckoned that the dangers of India defaulting on its international payments' obligations were on the rise.

Fresh moves to sell or pledge gold were put on hold as the government began deliberating what impact this would have on India's credit rating, which could have other adverse repercussions as well.

A meeting of secretaries, attended by Cabinet secretary Naresh Chandra, took stock of the situation on June 6. The fear was if any such step was taken, the Non-Resident Indians, who had parked Rs 20,000 crore (Rs 200 billion) of deposits in India, could start pulling out that money, aggravating the foreign exchange crisis.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

Indeed, on June 7, Sinha and Rangarajan issued a public statement assuring the nation that there would be no further pledging or sale of gold. But these, as subsequent events showed, were only statements aimed at assuaging the markets.

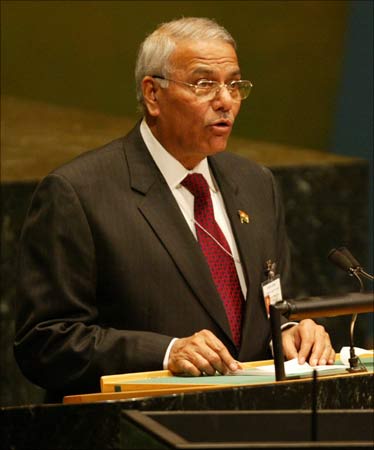

So, when Manmohan Singh took charge of the finance ministry on June 24, the tasks for him were unusually onerous.

He had a team in the finance ministry (Shukla and Nayyar) which had already done a lot in averting a default, but now the job was even more challenging. He had to put in place a new policy framework that would unshackle the economy to help it realise its inherent growth potential.

He held several rounds of meetings with his top team in the finance ministry. He did consult Montek Singh Ahluwalia, who was commerce secretary then, but those meetings would be held separately and not in the finance ministry.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

There was also Rakesh Mohan who was then in the industry ministry as its economic advisor, providing key inputs to the formulation of the industrial policy that would finally be unveiled at the time of the Budget.

The action plan became clear: the international community, including the World Bank and IMF, had to be told that India meant business and would take the toughest of measures to bail itself out of the crisis.

Prime Minister P V Narasimha Rao played a major role in that he gave his finance minister complete freedom to do what he thought was good for the Indian economy.

Exactly a week later, the plan to depreciate the Indian rupee was finalised. The idea was to depreciate the currency by 20 per cent, but the question was whether it should be done in one stroke or two phases.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

RBI was in favour of going through with the measure in one stroke, while the finance minister preferred a two-phase move, for that would allow people to absorb the shock. And that is exactly how it happened.

RBI explained the 9.5 per cent depreciation as a routine adjustment. The finance minister denied that it was done under pressure from IMF.

"We will not do anything under pressure and which is not consistent with our national interest," said Singh.

Industry's reaction was interesting. The Confederation of Engineering Industry, as CII was known then, welcomed the move, but Lalit Mohan Thapar, the chairman of the Thapar group, was the most illuminating: More steps should follow towards liberalisation and other long overdue measures.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

Political management was also on in full swing. Commerce Minister P Chidambaram held a meeting with media representatives explaining the logic of the move and outlining how the government was planning major structural reforms and would soon offer fiscal incentives for exports.

A day later, another round of currency depreciation took place -- this time by 11 per cent. In the space of three days, the Indian rupee's exchange value vis- -vis the US dollar moved down from Rs 21.09 to Rs 25.95.

Singh held a press conference and said that there would be no further depreciation of the Indian currency. The following day, Chidambaram unleashed a series of trade policy changes -- starting with the abolition of the cash compensatory support scheme to removal of supplementary licences, decanalisation of most import items and a transition from the replenishment licence scheme to a new system of tradeable exim scrips.

In short, a completely new trade policy regime was in place.

. . .

The INCREDIBLE 2 months that changed India forever

Photographs: Reuters

Even as these measures helped strengthen the economic policy framework, Singh had to go in for three more rounds of gold pledging, just to make sure India did not default.

On July 6, India air-freighted 25 tonnes of gold to London, to be kept with the Bank of England as security against which it obtained a commitment of a $200 million assistance. A week later, 9.8 tonnes of gold, and on July 18, 12 tonnes of gold were shipped to London with the same purpose.

India could now borrow up to $400 million against the pledging of about 47 tonnes of gold. The last round of shipment took place on July 18.

Six days later, Singh presented a Budget that changed the face of the Indian economy, not so much because of the fiscal policy directions, but for the new industrial policy that was unveiled in Parliament the same day.

That marked a new dawn for India.

article