| « Back to article | Print this article |

Don’t tinker with your long-term investment plan. But it is always better to make some critical changes, based on new tax laws and instruments

The start of a new financial year is a good time to review your financial plan and take stock of where you stand in relation to your goals.

If new goals have emerged, this is the time to make fresh investments for these.

While having a steady approach is a virtue here, make some adjustments in the light of developments that have occurred over the past year.

Equity funds

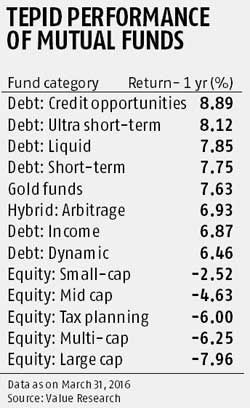

Large-cap funds have fared worse than mid-cap and small-cap ones over the past one year (see table).

Over this period at least, the conventional wisdom that large-cap funds tend to be more resilient than mid-cap and small-cap ones in a declining market was overturned. Nilesh Shah, managing director, Kotak Mahindra AMC, offers three reasons.

“For the bulk of the previous year, FIIs were sellers of large-cap stocks, whereas domestic institutional investors were buyers of mid- and small-caps. Large-cap stocks are also more linked to global sectors like metal and oil, whereas mid- and small-caps are linked to domestic sectors.

The latter has done better than the former, leading to stronger performance by mid- and small-cap stocks. Large-cap stocks’ earning growth decelerated or remained subdued throughout last year while mid- and small-caps delivered better growth,” he says.

Despite last year’s anomalous performance, investors should continue to have the bulk of their core portfolio, 70-75 per cent, in large-cap funds for stability, and only 20-25 per cent in mid-cap and small-cap funds.

Large-caps could also fare better in the near future.

Says Ashish Shankar, head of investment advisory, Motilal Oswal Private Wealth Management: “IT, pharma and private banks, whose earnings have been growing, will continue to do so. Public sector banks and commodity companies, whose earnings have been bleeding, will not bleed as much.

Many might even turn profitable.

FII flows turned positive this month and FIIs prefer large-caps.

With the US Fed saying it won’t hike interest rates aggressively, global liquidity should improve. If FII flows continue to be stable, large-caps should do better.” Valuations of large-caps are also more attractive.

Debt funds

Among debt funds, the category average return of income funds and dynamic bond funds was lower than that of short-term, ultra short-term and liquid funds (see table).

Explains Shah: “Last year, while Reserve Bank of India cut policy rates, market yields didn’t soften as much. The yield curve became steeper.

The short end of the curve came down more than the long end, which is why shorter-term bonds did better than longer-term gilts.”

Stick to funds that invest in high-quality debt paper, in view of the worsening credit environment. Shankar suggests investing in triple ‘A’ corporate bond funds.

“Today, you can build a triple ‘A’ corporate bond portfolio with an expected return of 8.5 per cent. Many of these have expense ratios of 40-50 basis points, so you can expect annual return of around eight per cent.

"If bond yields come down, you could end up with returns of 8.5-9 per cent. If you redeem in April 2019, you will get three indexation benefits, lowering the tax incidence considerably.” Investors who have invested in dynamic bond funds should hold on to these.

“A rate cut is expected in April. Yields will drop and there may be a rally in the bond market,” says Arvind Rao, Certified Financial Planner, Arvind Rao Associates.

Traditional fixed income

Traditional fixed income

The recent cut in small savings has jolted conservative investors.

The rates on these have been linked to the average 10-year bond yield for the past three months.

These will be revised every quarter now, make them more volatile.

“People who want to invest in debt and want sovereign security should continue to invest in Public Provident Fund.

No other instrument gives a tax-free return of 8.1 per cent with government security,” says Rao.

As for time deposits, financial planner Arnav Pandya suggests, “From April, fixed deposits of banks will give better returns than those of the post office.

"Decide on your investment tenure, see which bank is offering the best rate for that tenure, and invest in its deposit.”

Lock into current rates fast, as even banks are expected to cut their deposit rates.

Tax-free bonds are another good option. Nabard’s recent issue carried a coupon of 7.29 per cent for 10 years and 7.64 per cent for 15 years.

Beside getting tax-free income, investors stand to get the benefit of capital appreciation if interest rates are cut.

“People who have some risk appetite may also look at debt mutual funds and fixed deposits of stable companies,” adds Rao.

Gold

The sharp run-up in gold prices over three months, owing to the rise in risk aversion globally, took most people by surprise.

The sudden spurt emphasises the need to stay diversified and have a 10 per cent allocation to the yellow metal in your portfolio.

However, instead of using gold Exchange-traded funds, which carry an expense ratio of 0.75-1 per cent, invest via gold bonds, which offer an annual interest rate of 2.75 per cent.

The Budget made gold bonds more attractive by exempting these from capital gains tax at redemption.

Tax planning

Start investing in tax-saving instruments from the beginning of the year.

“Don’t leave tax planning for the end of the year, otherwise you may have to scramble for funds,” says financial planner Ankur Kapur of ankurkapur.in. For those with the money, Pandya suggests: “Invest the entire amount you need to in PPF before the April 5.

That will take care of tax planning for the year and you will also earn interest on your investment.”

Investors with a higher risk appetite could start a Systematic Investment Plan in an Equity Linked Savings Schemes fund, which can give higher returns.

“If you invest early in the year via an SIP, you will reap the benefit of rupee cost averaging,” says Dinesh Rohira, founder and Chief Executive Officer, 5nance.com. Pankaj Mathpal, MD, Optima Money Managers suggests linking all tax-related investments to financial goals.

If you live in your parents’ house and pay rent to them to claim House Rent Allowance benefits, which is perfectly legal, get a rent agreement prepared.

With 40 per cent of the National Pension System corpus having been made tax-free at withdrawal in this Budget (the entire corpus was taxed earlier), this has become more attractive.

“Open an NPS account if you have not done so already and enjoy the additional tax deduction of Rs 50,000,” says Anil Rego, CEO & founder, Right Horizons.

In view of the low returns from annuities, into which 60 per cent of the final corpus must be compulsorily invested, don’t invest more than Rs 50,000.

Tax deduction under Section 24 is available on the interest repaid on a home loan. “Buying a property to avail of the benefit is not advisable if the family has a primary residence,” says Rego.

Insurance

While reviewing your financial plan, check if the term cover is adequate.

A family’s insurance cover should be able to replace the breadwinner’s income stream. Financial planners take into account household expenses, goals like children’s education and marriage, and liabilities like home loans when deciding on a person’s insurance requirement.

“If goals have changed or liabilities have increased, raise the amount of cover,” suggests Mathpal.

Kapur says the premium rate is likely to be lower if you buy the term plan before your birthday.

Your health insurance cover might also need to be raised to take care of medical inflation.

The same holds true for household insurance if you have reconstructed your house and the structure has become more expensive, or if you have added expensive assets.

Rohira suggests buying add-on covers like accidental insurance and critical health insurance for comprehensive protection.

CHANGES YOU NEED TO MAKE

Investment

Insurance

Tax planning

The image is used for representational purpose only. Photograph: Reuters