Home buyers 40 years back had a completely different profile: they were in their mid-forties or older and most dipped into their provident fund corpus and other savings to fund a house.

Home buyers 40 years back had a completely different profile: they were in their mid-forties or older and most dipped into their provident fund corpus and other savings to fund a house.

D B Remedios was the first borrower of HDFC, which was the first organised player in the home loan market.

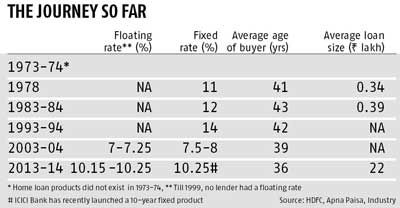

Remedios took a Rs 30,000 loan at a fixed rate of 10.5 per cent in 1978.

The amount was less than half the total amount of Rs 70,000 that he spent to build a house in Mumbai's Malad.

Today, the minimum that most borrowers seek is 65-80 per cent of the purchase amount.

Some still want even more despite the cap prescribed by the housing finance regulator, National Housing Bank (NHB) and the Reserve Bank of India (RBI).

Home buyers 40 years back had a completely different profile: they were in their mid-forties or older and most dipped into their provident fund corpus and other savings to fund a house.

For most, taking a loan was an alien concept, partly because of the social milieu and partly because access to loans was a difficult proposition.

In sharp contrast, home buyers now are younger - in their early thirties - and can put up much less of their own capital initially.

So, loan-to-value ratios are substantially higher. And home loans have become an essential part of their lives.

The evolution of the Rs 9-lakh crore or Rs 9 trillion (outstanding credit as on March 31, 2014) Indian home loan market is largely a tale of three institutions: HDFC from 1978, ICICI Ltd (now merged with ICICI Bank) from 1999 and State Bank of India from 2009. All three either introduced or aggressively pushed concepts that turned the market on its head.

While HDFC introduced the concept of housing finance, ICICI brought aggression into the market through the floating rate concept from 2000 (HDFC had this product earlier but there wasn't much traction).

SBI pushed the teaser rate (fixed-cum-floating) through its network of branches, the largest in the country.

In early 1970s, there was nothing called a housing finance market. "If you knew the banker or were a corporate client, you could raise money to build a house," says a former banker.

So when H T Parekh, former ICICI chairman and paternal uncle of Deepak Parekh, started HDFC, it was a welcome step.

HDFC later helped the government and other public sector entities set up SBI Home Finance, Canfin Home Finance, GIC Housing Finance and Gruh Finance.

Even foreign banks like Citibank entered the market in the 1980s catering to premium clients and services by providing doorstep delivery (in which bank officials visited the customer instead of the other way round) and introduced the concept of loan against property.

If the home loan market took a big leap in 1999, the credit goes to ICICI which changed the name of the game with its floating rate loans in early 2000.

"Banks and financial institutions were borrowing short-term and lending long-term, leading to a huge asset-liability mismatch," says a banker.

And customers lapped up floating rates because of the promise of paying less interest if rates came down. It was also a great time as rates were at their lowest. Some banks were offering fixed rates of 7.5 per cent in 2003. Floating rates were as low as 7 per cent or even less.

People were willing to borrow but not lend to us: Deepak Parekh

People were willing to borrow but not lend to us: Deepak Parekh

When we started 36 years ago, HDFC was a solitary player in the formal housing market.

Our only competition was from national, state and cooperative entities.

The housing sector at that time was considered as a non-productive sector and it received little, if any, government funding.

Individuals, typically, funded their purchases by their accumulated savings combined with retirement and provident fund drawdowns.

And they only came to a financial institution to bridge the gap.

There was no competition in the first 10-12 years.

There were no recovery laws. We could only file a civil suit if there was a default.

The cost of litigation was more than the value of loan. But the biggest challenge was how to raise money.

When we advertised, we had hordes of people coming to us for money. But we had no one giving us money.

No one trusted us with money though they were willing to borrow from us.

For the first 10 years, we had to depend on wholesale funding to fund retail. Subsequently, we started getting retail investors.

We had to go to banks, IFC gave us the first line of credit and LIC gave us Rs 10 crore in those days.

The challenge was to raise money and manage crowds who were waiting for hours because they wanted loans.

Today, the housing sector in India is in a sweet spot as there is inherent demand to buy a house by a young population with steady jobs in an under-penetrated market.

A lot of players have entered this sector in the past two decades offering easier and flexible financing options.

Product differentiation, as a result, is no real differentiator. Interest rates, though an important factor in the entire value chain, are only one link. So, what really differentiates is the quality of customer service and value addition.

Product differentiation, as a result, is no real differentiator. Interest rates, though an important factor in the entire value chain, are only one link. So, what really differentiates is the quality of customer service and value addition.

An ICICI old-timer recalls how Chairman K V Kamath walked out of a meeting to decide on the launch of the home loan product after he was told that the lender would achieve half of HDFC's annual sales in five years.

The team took the cue and reworked the projection substantially.

In another meeting he said that his main worry was the day SBI woke up to the potential of home loans.

It took almost a decade for SBI to wake up, but it did so in style. In 2009, then chairman O P Bhatt disrupted the market by launching the teaser rate - 8 per cent in the first year, 9 per cent in the next two years and a market-linked rate for the rest of the tenure .

With a CASA (low-cost deposits) of 47.58 per cent, Bhatt could afford to do it.

Others followed suit after shedding their initial reluctance.

For example, HDFC Chairman Deepak Parekh called it a gimmick but was forced to launch a similar product.

The huge success of teaser rates, however, drew the Reserve Bank of India's ire. And one of the first things that Pratip Chaudhuri, Bhatt's successor at SBI, did was to discontinue the product.

Many banks, which could not compete on rates, tried to attract customers by giving a higher loan-to-value in the garb of home improvement or other kinds of loans.

So, some banks or finance companies gave as much as 110 per cent or 120 per cent of the purchase amount.

The RBI has now capped the loan-to-value limit at 80 per cent for banks and they cannot pay registration and stamp duty charges. However, NBFCs can continue to include the latter while giving a home loan.

Of course, one thing still hasn't changed. New borrowers continue to get lower rates than existing borrowers.