| « Back to article | Print this article |

While prices sustaining lower levels is crucial, govt actions are also a key monitorable given the forthcoming elections in 2024.

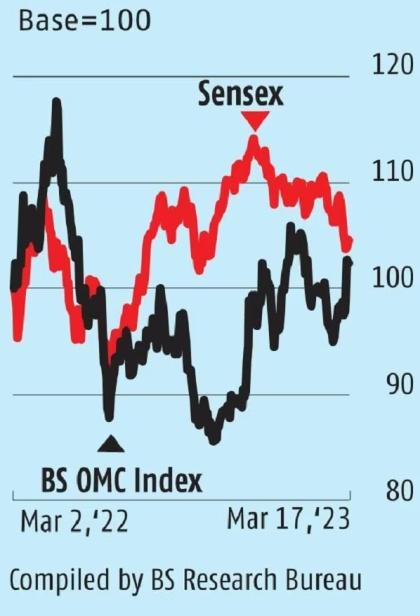

One consequence of the recent turmoil in global banking has been a sharp drop in commodity prices.

Oil, in particular, has seen a dip with most analysts focussed on likely fall in global demand.

Although this is an early reaction, it could be a trend.

On the other hand, OPEC+ (OPEC members plus Azerbaijan, Bahrain, Brunei, Kazakhstan, Malaysia, Mexico, Oman, Russia, South Sudan and Sudan which are oil-exporters but not OPEC members) is running production at below target. Hence, cuts in supply could stabilise oil prices or slow a downtrend.

The impact of lower prices on India is generally positive given 85 per cent of crude and over 50 per cent of gas is imported.

The impact on the refining and PSU oil marketing companies (OMCs) is likely to be a positive one.

On the other hand, a fall below $75 per barrel would hurt margins for ONGC and Oil India (OIL) as net of Windfall Tax, net crude realisation for both falls to $76 per barrel.

Every subsequent decline of $1 in crude line leads to a negative 2-3 per cent impact on the earnings of both firms.

The immediate impact of lower crude prices on OMCs is that the average gross marketing margin (GMM) is now around a positive Rs 10 per litre, which is a big turnaround from a negative GMM Rs 6.8 per litre across the first three quarters of the 2022-23 financial year (FY23).

This is well above the historical GMM of Rs 3.5 per litre.

It should help a partial turnaround from aggregated losses of approximately Rs 50,000 crore over the first nine months of FY23.

The FY24 Budget provides for capital support of Rs 30,000 crore to OMCs for emission-reduction-related capex.

Historically, the government has usually absorbed 50-65 per cent of under-recoveries and asked upstream PSUs to bear the balance, with OMCs either exempted or given a limited 1-3 per cent burden as the interest cost of funding delay in government compensation.

The government increased SAED/windfall taxes on domestically-produced crude by Rs 50 per tonne, to Rs 4,400 per tonne ($7.5 per barrel) on March 4, but this could be reviewed given that crude prices have fallen since then.

If we assume zero compensation for under-recoveries, it would take OMCs around 2-3 quarters to fully recoup losses if they can maintain the current GMM.

However, apart from the chances of normalisation of margins for global reasons, investors must also bear in mind that the next fiscal is an election year and this could mean retail prices being held low.

The optimism on OMCs is therefore conditional on crude below $75 per barrel and government allowing OMCs to recoup past losses by maintaining high GMM.

Asian spot LNG prices also continued to go down, hitting the lowest levels since July 2021, due to tepid demand and higher inventory.

Prices are expected to remain sluggish on the back of higher inventory levels in Europe, the restart of US's largest Freeport LNG terminal and strong renewables generation, and above all, global slowdown.

However, China imports are also rising and that could stabilise the price trend.

Analysts have now switched sides to give 'buy' ratings to HPCL (target price or TP of Rs 260 in one case) and BPCL (TP of Rs 390).

However, IOC has aggressive capex plans which will negatively impact TP.

ONGC, meanwhile, is a beneficiary as majority shareholder of HPCL.

The stock of BPCL has jumped Rs 20 to touch Rs 351 in the last week while that of HPCL is up Rs 15 to Rs 242.

Feature Presentation: Rajesh Alva/Rediff.com