If the Reserve Bank of India does cut the repurchase rate substantially, the uptrend would gain steam. If it doesn't, serious selling pressure may develop again, says Devangshu Datta.

The contrast between higher gross domestic product (GDP) growth estimates and lower corporate earnings presents a continuing riddle.

Provisional estimates from the Central Statistical Office claim GDP grew at 7.3 per cent in 2014-15.

The Q4 growth rate (January-March 2015) was 7.5 per cent year-on-year (y-o-y), while the Q3 (October-December) growth rate was 6.6 per cent y-o-y.

Agriculture was flat at 0.2 per cent for the fiscal. Industry and services grew at 6.1 per cent and 10.2 per cent respectively.

The value-added method of estimating GDP places stress on numbers sourced from corporate balance sheets in the database of the Ministry of Corporate Affairs.

The GDP numbers suggest that the corporatised elements - industry, services - did well and logically, corporate earnings should have been good in the second half.

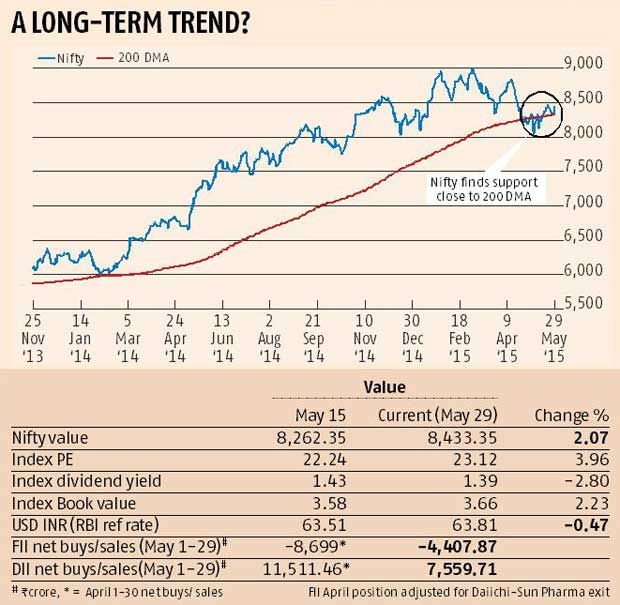

Now, let's look at the Nifty index. Those 50 large stocks represent about two-thirds of total market capitalisation on the National Stock Exchange.

In Q3, there was a 7 per cent drop in aggregate net profits.

In Q4, 43 Nifty companies have declared results so far. Of these, 23 companies had declines in net profit, or outright losses.

Aggregated net profits for 43 was 14 per cent lower, excluding exceptional impairments (Tata Steel, Vedanta). Unadjusted, net profits dropped 51 per cent.

Aggregated net profits for 43 was 14 per cent lower, excluding exceptional impairments (Tata Steel, Vedanta). Unadjusted, net profits dropped 51 per cent.

In a broader corporate set, Q4 has seen sales dip slightly lower and profits run flat across 500-odd listed companies. In Q3, net profits dropped 8 per cent for a set of 1,300 listed companies, while sales grew 2.5 per cent.

It is difficult to reconcile those numbers to GDP estimates. Assuming estimates are accurate, it is hard to find stocks with decent growth and valuations.

Small to medium unlisted businesses must have delivered extraordinary performance to compensate for the washout in big stocks.

But there's little sign of that "bottom-driven" rebound.

The banking sector results suggest muted growth. Credit grew 12.6 per cent in the last fiscal, the lowest growth rate in 18 years. In April 2015, credit growth slowed to 10.5 per cent.

The chairperson of the State Bank of India (SBI), which contributes about 16 per cent of total credit across all sectors, says she believes growth will not pick up until January-March 2016.

SBI saw credit growth at just 7.25 per cent, while it restructured a massive Rs 28,000 crore or Rs 280 billion of loans in the fiscal, including Rs 11,000 crore restructured in Q4.

Gross non-performing assets (NPAs) amount to 4.25 per cent of total advances. NPA plus restructurings rises above 8 per cent.

If that is representative of averaged bank performance, it does not inspire much confidence.

Anyhow, the market sentiment remains optimistic because the Reserve Bank of India (RBI) is expected to pitch in with its third rate cut of 2015 at its policy meet on Tuesday.

Foreign portfolio investors (FPIs) were net sellers in rupee equity and debt through May.

FPIs did buy on last Friday, and domestic Institutions, including mutual funds, have made substantial equity and debt investments through May.

Inflation at 4.87 per cent (April, consumer price index) and -2.65 (wholesale price index) is well below target. The Index of Industrial Production was weak at 2.3 for 2014-15 fiscal.

The real rate of interest is 2.5-3 per cent. The RBI, therefore, has room to cut decisively. There is strong consensus that it will do.

On the external front, the US revised its January-March 2015 GDP estimates downwards to claim a contraction of 0.7 per cent.

Traders hope that this will mean a postponement of the US Federal Reserve's threat of hiking policy rates.

The European Central Bank may step up its bond-buying programme. Greece still seeks a bailout.

Technically, the Nifty has range traded in the region of its 200-day moving average (DMA), which most analysts reckon is a reliable indicator of the long-term trend. It lifted above the 200 DMA on Friday.

This suggests that the big bull market is alive, if not exactly kicking. If the RBI does cut the repurchase rate substantially, the uptrend that started on Friday would gain steam.

If the RBI does not cut, serious selling pressure may develop again.