| « Back to article | Print this article |

Policymakers should consider the challenges of beneficiary identification, distributor opposition and beneficiary financial inclusion.

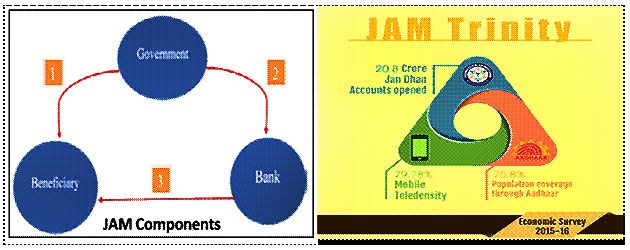

The Economic Survey 2015-16 presented on Friday in the Parliament by the Union Finance Minister Arun Jaitley emphasises that JAM Trinity - Jan Dhan, Aadhaar, Mobile - can help government to implement large-scale, technology-enabled and real-time Direct Benefit Transfers (DBTs) to improve economic lives of India’s poor.

First variety of Jam Pahal scheme of transferring LPG subsidies via DBT - has reduced leakages by 24 per cent.

Economic Survey suggests that while deciding where next to spread JAM, policymakers should consider the challenges of beneficiary identification, distributor opposition and beneficiary financial inclusion.

Spreading JAM to other areas will reduce leakages and provide more fiscal space to the government.

JAM components:

Economic Survey divides JAM into three components:

1. Identification or First-Mile: Identification of beneficiaries by government

2. Transfer or Middle-Mile: Transfer of fund to beneficiaries by government

3. Access or Last-Mile: Access of fund by beneficiaries

Identification:

First-mile deals with identification of beneficiary. This layer has issues of ghost and duplicate names due to administrative and political discretion and use of pre-Aadhaar database.

It is easier to implement the JAM for universal scheme than targeted one as identification will be easier.

Identification of household-individual connection is important to note here as some schemes target at household level like JDY and some at individual level like Aadhaar. Aadhaar can help in better identification of the beneficiaries.

Transfer:

Middle-mile deals with the challenges of payment where government transfer benefits to the banks. But lack of bank accounts and its information with government put hindrances in the middle-layer connectivity. Main issue in this layer is of within-government coordination and dealing with supply chain interest groups. Jan Dhan can help beneficiaries to have bank accounts.

Access:

Last-mile layer faces issues of lesser Bank penetration, mostly in rural areas. It deals with actual transfer of money from Bank to Beneficiary accounts. It also deals with issues of exclusion of genuine beneficiaries. Mobile can inform about benefits and also allow easier fund transfer.

Where next to spread JAM?

Economic Survey argues that policymakers should decide where to apply JAM based on two considerations of:

1. Amount of leakages

2. Control of the central government

If amount of the leakages in a given scheme/area is huge then it can be next target for introduction of JAM as subsidies with higher leakages will have larger returns from introducing JAM.

Similarly control of central government will reduce administrative challenges of co-ordination and political challenges of opposition by interest groups.

Based on these two criteria- leakages and central government control-Survey suggests fertilizer subsidies and within-government transfers as two most promising areas for introduction of the JAM.

JAM Preparedness Index:

Further economic survey has formulated JAM-Preparedness Indices for Urban and Rural areas in each state.

It uses Aadhaar penetration, basic bank account penetration and Banking Correspondents (BC) density as indicators for the indices.

It has also prepared Biometrically Authenticated Physical Update or BAPU-Preparedness Index, using Aadhaar penetration and Point of Sale machines as indicators, for each state and has compared Rural-JAM Preparedness Index with BAPU-Preparedness Index.

It has found that many states are having higher scores in BAPU-Preparedness Index as compared to Rural JAM-Preparedness Index.

Thus it suggests use of BAPU as short-term solution to reduce the leakages in these states, till states are well prepared for introduction of the JAM.

Conclusion:

Introduction of DBT in LPG and MGNREGS have proved that use of JAM can considerably reduce leakages, reduce idle funds, lower corruption and improve ease of doing business with the government.

Despite huge improvements in financial inclusion due to Jan Dhan, JAM Preparedness indicators suggest that there is still long way to go.

Centre can invest in last-mile financial inclusion via further improving BC networks and promoting the spread of the mobile money. In the meantime models like BAPU can be used as an alternative to reduce the leakages.

Text: Press Information Bureau