'Global investors expect the rupee to be more vulnerable in the downturns in the future than ever before,' notes Apoorva Javadekar.

Illustration: Uttam Ghosh/Rediff.com

The Indian rupee is trading above the 73 mark against the dollar and it is down over 15 per cent year-to-date.

It is true that most of the emerging markets have depreciated this year -- rising yields in the United States, increased uncertainty due to a trade war, and a risk-off mood that set in after news from Turkey and Argentina could be some of the common factors underlying this fall.

But the Indian currency is one of the worst hit.

The Mexican peso is surprisingly trading around the same level where it was at the start of the year -- around 19 per dollar -- while the Taiwanese and Malaysian currencies have depreciated less than 3 per cent year-to-date.

A lot has been written in the media over the last month about the pros and the cons of rupee depreciation.

But a more fundamental question remains unanswered -- is the rupee fairly valued or does the current fall reflect undervaluation?

I look at the rupee as an asset class to answer this question.

The equity premium (equity returns in excess of risk-free rate) averaged around 6 to 7 per cent in the US over the last 100 years.

What is the precise risk in the equities that investors require premium to hold it?

Corporate performance and hence the equity income (dividends, for example) are highly correlated with the overall economy.

Investors can't rely on equities to smooth their income profile.

In fact, equities would make your income profile volatile and hence investors require the risk-premium to hold the equities.

The corresponding measure of risk-premium in the currency markets is carry-profits -- profits earned by borrowing in dollar, investing in India at risk-free rate and reconverting the proceeds back to dollar in the future to clear off the loan.

Because reconversion rate from rupee to dollar is not known at the time of investment, carry-strategy is risky and an investor requires risk-premium to invest in such a strategy.

This is Eugene Fama's insight.

A simple hypothesis such as the Uncovered Interest Parity (UIP) suggests that countries with high interest rates should depreciate in the future so as to wipe out any easy money-making opportunities in the efficient market.

The problem with the hypothesis is that it completely ignores the risk-premium view.

Mr Fama in his famous 1984 paper showed that actually many of the high interest rate currencies appreciate in the future and others do not depreciate as much as predicted by UIP.

The under-depreciation relative to the UIP reflects carry-profits or the risk-premium in the currency markets.

So, what's the extent of the risk-premium or carry-profits in the rupee-dollar markets historically?

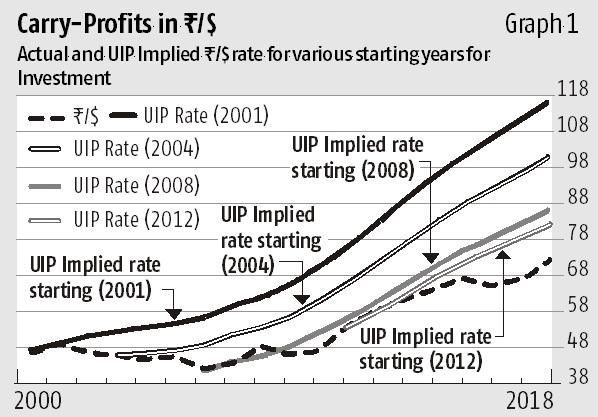

If one would have initiated the rupee-dollar carry strategy in 2001 and held it till today, it would have earned him annual returns of 2.70 per cent.

Average interest differential between India and the US has been 5.21 per cent and the rupee depreciated by 2.35 per cent annually since 2001, giving net returns of roughly 2.70 per cent.

A more interesting way to state this fact is that the rupee-dollar carry trade would have earned zero profits if the current rupee-dollar rate would have been Rs 118/dollar.

Hence, global investors required 2.70 per cent risk premium annually to invest in the rupee.

Graph 1 shows that in fact, the rupee-dollar carry trade initiated during any year has yielded positive profits -- the carry-trade has never been under-water for more than a year.

Hence, the key to value the rupee is to tell whether 2.70 per cent is a reasonable risk-premium.

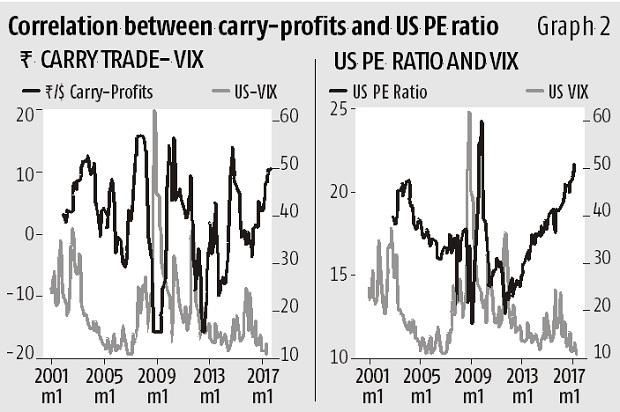

Graph 2 shows that carry profits are highly correlated with US equity market Price-Earning ratio and both are negatively correlated with the US VIX -- the fear index.

In other words, the rupee exposes the US investor to the same risk as the US equities -- the risk that both the assets are positively correlated with the broader economy and provide a poor hedge to the investor's income profile.

Hence, prima facie, it looks that there is a reasonable risk-factor that is being priced in the Indian currency.

Hanno N Lustig (Stanford) and Adrien Verdelhan (MIT) in their 2007 American Economic Review paper using cross-country data compute that a unit increase in the currency beta with respect to the US growth increase the carry-profits by roughly 2.5 per cent.

I measured the rupee's beta with respect to the US consumption growth and it is around 1.

Hence, a risk premium of roughly 2.5 per cent is a reasonable one for the rupee, suggesting that the rupee has roughly stayed aligned with the risk-premium view over last two decades.

How to interpret current rupee depreciation within this framework?

More depreciation now implies lower depreciation or may be appreciation in the future implying higher carry-profits in the future.

In short, the risk-premium on the rupee just went up and much more than other EM currencies.

That means global investors expect the rupee to be more vulnerable in the downturns in the future than ever before.

One interesting way to link this view to more fundamental indicators such as fiscal deficit is to observe that higher fiscal deficits put an upward pressure on the domestic interest rates by grabbing the limited domestic savings.

But higher interest rates reflect carry-profits and the risk-premium in the currency markets.

One reason why foreigners care about fiscal deficits is as follows: Poor fiscal health means higher government borrowing, potentially foreign borrowings, during tougher times when tax revenues are lower.

But this means that the domestic currency will depreciate during tough times if a government demands foreign currency.

This is exactly the risk (beta risk) that is priced in assets from equities to currencies as argued before.

In short, fiscal math is important even within a risk-premium view!

Apoorva Javadekar is research director, Centre for Advanced Financial Research and Learning.