Abheek Barua believes India is protected from the 'downside' that emerging markets might face, but is likely to ride the upside when the EM boat rises.

The economist's insight into the global and domestic economy at the turn of the financial year.

And for a hundred visions and revisions,

Before the taking of a toast and tea

-- T S Eliot, The Love Song of J Alfred Prufrock

The end of the first quarter of the calendar year is a time when economic forecasters like me take a hard look at the predictions made at the beginning of the year and figure out where exactly their tea leaves let them down. In fact, there is much to revise in both the assumptions and forecasts we made both about the global and domestic economy.

For one thing, contrary to what a fair number of my ilk had assumed, the United States economy and financial markets are not acting as a giant vacuum cleaner sucking money out of all other markets and asset classes and driving the dollar up as a result.

Two things are responsible.

First, despite clear signs of sustained growth and a pick-up in consumer inflation, the American central bank -- the Fed -- does not seem too keen to accelerate the pace of monetary tightening. In its March 15-16 policy meeting, the members of the rate-setting open market committee stuck to its earlier forecasts for interest hikes, suggesting de-facto that they intend to go slow and steady.

Second, markets are beginning to discount US President Donald Trump's somewhat wild forecast of 4 per cent growth based on massive fiscal expansion (and a consequent rise in both deficit and debt). While he has presented an outline for his budget, it is likely that the more grandiose plans will get thwarted by the nation's legislators on Capitol Hill. Pushing through policy proposals might be a tad more difficult than firing contestants from The Apprentice.

The US is likely to grow, if median forecasts are to be believed, at around 2.5 per cent -- certainly a respectable number, but nowhere close to what the so called "Trump trade" had factored. Thus, the US seems to be in the clichéd Goldilocks scenario -- neither hot nor too cold -- the economy is picking up gradually, consumer and business sentiment is good and the Fed's playing ball.

The implications are the following.

The wedge between the US and other interest rates will not be big enough to drive the dollar up too sharply and we might see it decline against other currencies for a bit.

Improving US growth might push the US stock market a little further up from the stratospheric levels that they have reached, but there will be enough investment funds seeking other markets.

Europe has produced its share of surprises as well. Its political situation has come as a relief as the possibility of Brexit setting off a domino effect seems to be receding.

The Dutch did not choose the Islamophobic, anti-EU Geert Wilders as their prime minister in their elections a couple of weeks ago.

France, which is due to go in for elections in April, finally seems to have found a worthy opponent in Emmanuel Macron to the euro-basher, Marine Le Pen.

The German elections due later this year are likely to be a "shoo in" for the pro-euro coalition currently in power.

Thus, the euro project seems alive and well contrary to some of the year-start forecasts that saw it falling below parity to the dollar, it has gained and could gain further against the dollar. This is backed by improving performance in the region -- the last quarter saw a fairly healthy growth of 0.4 per cent (quarter on quarter, 1.7 per cent annualised) and with both consumer demand and exports doing well, growth in 2017 could be better.

Also read: The big picture

Economist: 'India will be world's fastest economy for the next decade'

Investor: 'FY18 will be tough for India's economy'

The improvement in external demand in Europe has a lot to do with buoyant demand from emerging markets.

This prima facie seems to suggest that they have pulled themselves up from the deep funk that they seemed to be getting into in 2016. Thus, the niggling worry that, with the US rate cycle turning, this bunch of markets would just fall off investors' maps has diminished.

China seemed to have accepted the fact that 6.5 per cent annual growth is their "new normal", and is getting on with life. There is some evidence that Chinese firms are borrowing in dollars again and are not being exhorted (or arm-twisted by the authorities) to refinance dollar loans in their local currency. This suggests that the government and central bank are less worried about the risk of an external loan crisis than they were a few months ago.

India appears to be in the sweetest of sweet spots as far as its financial markets go.

I think that it has partly delinked itself from the EM pack in the sense that it is protected from the "downside" that these markets might face, but is likely to ride the upside when the EM boat rises.

Investors seem to be happy with the fact that the government can take bold steps like demonetisation, the GST mess seems sorted, that there is political continuity, and a strong and visible leadership.

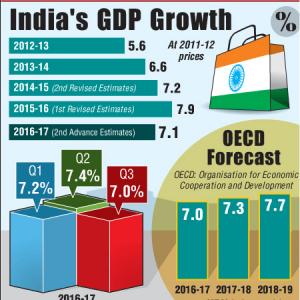

Some scepticism about recent GDP releases notwithstanding the general perception is that it will grow at a rate somewhere in the 7-per cent ballpark.

So far so good. But perception is known to be fickle.

For growth to sustain and then accelerate, private investment activity has to pick up. I get a sense that large companies will first take the inorganic route to add to capacity -- that is they would first be interested in picking up stressed assets first before they actually install capacity.

This is the perfect time to decisively solve our "bad loan" problem and free up bank balance sheets.

It is also time to take stock of how much programmes like Make in India have lived up to the government's own expectations.

There is a need to find concrete solutions to the gap between unemployment and headline GDP growth.

Finally, let's not forget the fact that positive sentiment also drives short-term capital flows into our markets that are far greater than we need. This brings with it the risk of currency overvaluation and inflation pressure.

No sleep then for the government or the Reserve Bank of India.

Abheek Barua is chief economist, HDFC Bank. The views expressed here are his own.

Scroll down for more insights into India's economy in 2017-2018.