| « Back to article | Print this article |

In part three of a series, Rangeet Ghosh, Aakanksha Arora, Sutirtha Roy and Arvind Subramanian explain how the big numbers obscure some serious deficiencies in the 'lifeline of the nation'

Part I: 5 vital questions on India's credit

Part II: Experts list few things that will be different in FY16

Link of the opening scene in the first part of Satyajit Ray's great Apu trilogy.

As the object of awe, wonder, and thrill for young Apu, the onrushing train is a majestic metaphor for escape, opportunity and connectivity.

That deep, intuitive, and dare we say romantic, case for the railways underlay the prime minister's speech in Varanasi last year when he spoke of the railways as the backbone of India's development.

That deep, intuitive, and dare we say romantic, case for the railways underlay the prime minister's speech in Varanasi last year when he spoke of the railways as the backbone of India's development.

But there is also the more prosaically rational case for the railways made in Chapter 6 (Volume I) of this year's Economic Survey.

To understand this case, consider the problem, symptoms, and consequences.

Today, the 'lifeline of the nation' operates over 19,000 trains carrying 23 million passengers, and over three million tonnes of freight per day.

But these big numbers obscure serious deficiencies, a major one being chronic under-investment.

The share of railways in total developmental expenditure has remained at less than 2 per cent since 1990s (whereas the share of roads and bridges has been at around 7 per cent).

The contrast with China is striking. Chinese investment in railways, especially over 2005-12, has been about 11 times higher in per-capita terms. As a result, China, which had lower capacity in 1990, overtook India by the mid-1990s and as of 2010, outstripped India by about 25,000-route km.

This problem of under-investment manifests itself in several symptoms.

This problem of under-investment manifests itself in several symptoms.

There is serious network congestion with 65 per cent of sections operating at above 100 per cent capacity.

With the same network being used by both freight and passenger trains and priority generally accorded to passenger traffic, average freight train speeds have almost stagnated between 2000-01 and 2012-13.

Not surprisingly, India lags behind both China and Russia in network productivity (as measured by net tonne per km/network length).

Another symptom of the problem is the ceding of considerable share of freight traffic to roads.

The modal share of Indian Railways in freight traffic has declined to around 33 per cent in 2011, and estimated to decline further to 25 per cent by 2020 if the current state of affairs continues.

The comparable numbers in China and Russia are significantly greater.

What are some of the consequences?

The substitution of railways by roads entails large private costs in the form of worsening competitiveness and significant social costs in terms of more accidents, greater mortality, congestion and environmental pollution, including higher greenhouse gas emissions.

Another consequence, which relates as much to policy choices as under-investment, is the impact on the economy's competitiveness.

Another consequence, which relates as much to policy choices as under-investment, is the impact on the economy's competitiveness.

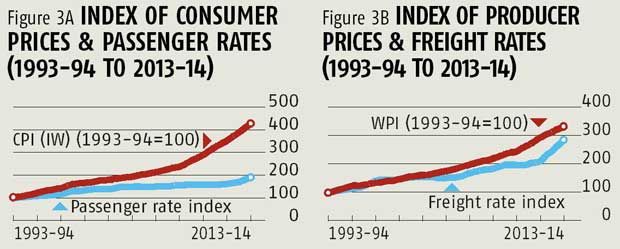

The Indian Railways has had to shoulder social responsibilities defined largely by the ability to provide cheap and subsidised passenger services.

Over the years, passenger fares have increased negligibly compared to freight rates, resulting in rates that are among the highest globally (in purchasing power parity terms).

The neglect of freight has dented the competitiveness of Indian industry, which is very logistics-intensive.

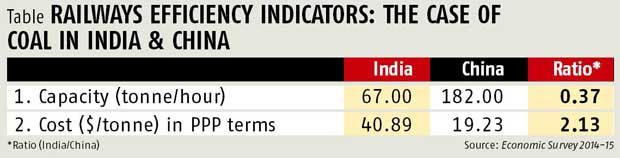

Indian Railways transports only about a third of the amount of coal transported in China per hour, and does so at more than double the cost. It is then not surprising that Indian manufacturing and exports become less competitive.

We know that the consequences of under-investment are substantial because our analysis shows that additional investments generate over-size returns.

Based on input-output tables, we estimate in the Economic Survey 2014-15 (Vol I, Chapter 6) that the large backward and forward linkages related to the railways generate a railways investment multiplier of about five.

Similarly, other econometric evidence suggests that public investment in the railways, would positively and durably affect levels of manufacturing and aggregate output, with multipliers of around five: that is, Rs 1-increase in railways investment is expected to boost economy-wide manufacturing output by Rs 5 over the medium term.

While under-investment is a major problem, there are perhaps even deeper influences such as organisational structure, legacy factors and incentives that need to be addressed, which have been discussed in several recent reports on the railways, including that of the National Transport Development Policy Committee (NTDPC 2014).

A good start towards turning around the railways was begun in the recent Budget under new and dynamic leadership.

There is a long road - or rather track - to travel but an auspicious beginning has been made.

One of the lesser known facts about Chinese history is the importance of railways to Deng Xiaoping's attempt to turning the economy around and ushering in the Chinese miracle.

After his third and final rehabilitation, he implemented famously the reform of Chinese agriculture. But after his second rehabilitation, he focused on improving the performance of the Chinese railways.

Should India and the government do for the Indian Railways what Deng did for China's railways?

Should the government do for Indian Railways what the previous National Democratic Alliance government did for roads via the Pradhan Mantri Gram Sadak Yojana and the National Highways Development Project (NHDP)?

Our analysis suggests that the answers to both the questions are resoundingly yes.

Ghosh is OSD to the chief economic advisor, Arora is assistant director in the Ministry of Finance, Roy is a Fulbright Scholar at the JohnsHopkinsUniversity, and Subramanian is chief economic advisor in the Ministry of Finance.