| « Back to article | Print this article |

Financial inclusion, concerns more than just a transactional bank account. It should address savings, loans, transactions, and insurance in order to best meet consumer needs, says Ashish Desai.

Providing banking services to the bankable unbanked has been on the agenda of central banks in most countries, particularly those of emerging markets.

Providing banking services to the bankable unbanked has been on the agenda of central banks in most countries, particularly those of emerging markets.

A significant section of the target customer base in emerging markets earns less than $2 a day and can ill-afford banking services, due to the high costs in the form of minimum deposit requirements and withdrawal rules that are generally associated with financial services.

A study commissioned by the World Bank estimates that bank branch penetration is 45 per cent among middle and high-income groups and less than 5 per cent among the low-income segment in emerging markets.

The demographic and credit profile of a large segment of the potential customer base in emerging markets hinders the growth of institutional banking at that segment.

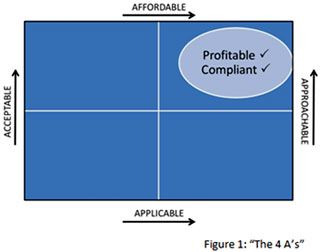

For people at the bottom of the pyramid, which I would rather address as mass market or emerging class; the primary challenge in accessing banking services are not just affordability but applicability and accessibility of services. To ensure that branchless banking works effectively, four verticals have to be considered: availability, applicability, acceptability and affordability; all in the context of the target market.

The kind of products and services offered need to ensure that the customer is enticed to purchase the service and that it is profitable. More so than others, customers of the emerging class are concerned that the products they buy are relevant to them. Financial inclusion, concerns more than just a transactional bank account. It should address savings, loans, transactions, and insurance in order to best meet consumer needs.

The kind of products and services offered need to ensure that the customer is enticed to purchase the service and that it is profitable. More so than others, customers of the emerging class are concerned that the products they buy are relevant to them. Financial inclusion, concerns more than just a transactional bank account. It should address savings, loans, transactions, and insurance in order to best meet consumer needs.

Distribution structures have to be designed so that they will help support the product, whether those are retail chains, self-service models or a blend of a physical franchisee chain, retail chain and self-service channels. Branchless banking is considered as a alternative to ensure effective and efficient accessibility.

As the penetration of mobile phones continues, remote payments and the idea of branchless banking is now gaining popularity; Especially in emerging markets, where a large number of individuals are unable to access banking services because conventional banking is expensive, relative to an individual’s income.

With the opportunities comes the challenges , especially with remote branchless banking where there is limited face time with the customer. Unlike internet banking or mobile banking , branchless banking in emerging markets has some unique characteristics:

With the opportunities comes the challenges , especially with remote branchless banking where there is limited face time with the customer. Unlike internet banking or mobile banking , branchless banking in emerging markets has some unique characteristics:

This in all probability is the first account of many customers. They have low financial literacy and will take while to come up the curve. It is imperative that the technology , operations and processes have got inherent security , checks and balances. The success of the branchless banking model hinges on the following drivers:

Most of the time branchless banking is viewed as setting up of distribution network for account opening , cash deposit, cash withdrawal and money transfer. However Branchless banking cannot be looked at in isolation of the product set offered. Idea of introducing branchless banking is to driver efficiency in operating cost and usage of account.

Most of the time branchless banking is viewed as setting up of distribution network for account opening , cash deposit, cash withdrawal and money transfer. However Branchless banking cannot be looked at in isolation of the product set offered. Idea of introducing branchless banking is to driver efficiency in operating cost and usage of account.

A customer will walk 5 km to get a loan while will walk 1 Km to open an account and 500 mts to do a transaction. If the distribution is not available , the account turns dormant as the accessibility of the account is impacted. Branchless banking can also drive efficiencies.

Operating cost of Micro Finance Institutions are higher , due to weekly or bi monthly physical collection of loans. A branchless banking network , where the customers can deposit the monies to do the repayment of the loan would help in addressing the cost of collection.

Banks complain, the cost of transaction is too high to service the small value transaction. The cost of branch banking service becomes too large for the emerging class to be serviced at the bank branch. Hence the alterative is branchless banking.

It is viewed as Branchless banking being a means and medium to empower customer at mass market level. But the pyramid has to inverted, not based on how many people are there , but what potential the segment offers. However another perspective is that it is necessary to increase the efficiency and reduce cost of a branch banking transaction rather than drive the mass market segment to alternative location. By providing branchless banking through Agent network , are we asking a section of society not to visit the branch? In the quest of focusing on empowerment are we forgetting the basic constitutional premise of equality.

Ashish Desai is Head - Consumer Banking, FirstRand Bank India